Every year, taxpayers in the United States are met with a myriad of tax forms, each serving a specific purpose in the realm of taxes. Among these, the 1098 tax form is crucial for individuals who pay interest on certain types of loans. This form is vital as it reports the amount of interest paid during the year, which can often be deductible on your tax return. Understanding this form is essential for maximizing your tax benefits and ensuring compliance with tax laws.

While tax forms can seem daunting, the 1098 tax form is relatively straightforward once you know its purpose and components. This form is primarily used by lenders to report mortgage interest of $600 or more received during the year in the course of their trade or business from an individual, including a sole proprietor. It's a tool that helps taxpayers claim deductions on their mortgage interest, student loans, and other relevant expenditures, potentially reducing their taxable income.

For many taxpayers, the 1098 tax form represents a significant opportunity to save on taxes. However, the key to benefiting from it is understanding its different types, how to accurately report the information, and how it fits into your overall tax filing strategy. This guide aims to demystify the 1098 tax form, providing insights into its different categories, the process of filing, and how taxpayers can leverage it effectively. Let's dive into the details to ensure you grasp everything there is to know about the 1098 tax form.

Table of Contents

- What is the 1098 Tax Form?

- Types of 1098 Tax Forms

- Who Needs to File a 1098 Tax Form?

- How to Fill Out a 1098 Tax Form?

- When Do You Receive a 1098 Tax Form?

- How Does the 1098 Tax Form Affect Your Taxes?

- Common Mistakes to Avoid with 1098 Tax Forms

- What Happens If You Don't Receive a 1098 Tax Form?

- How to Correct a Mistake on a 1098 Tax Form?

- Impact of 1098 Tax Forms on Mortgage Deductions

- Student Loan Interest Deductions and 1098-E

- Education Expenses and 1098-T

- Vehicle Donations and 1098-C

- FAQs About the 1098 Tax Form

- Conclusion

What is the 1098 Tax Form?

The 1098 tax form is a document used in the United States to report various types of interest and tuition expenses that may be tax-deductible. This form is provided by the entity to whom you paid the interest, such as a bank or educational institution. The primary function of the 1098 tax form is to assist taxpayers in preparing their tax returns by detailing the amounts paid that could potentially be deducted from their taxable income.

There are several variations of the 1098 form, each serving a different purpose. The most commonly used is the standard 1098, which reports mortgage interest payments. Other versions include the 1098-E for student loan interest, the 1098-T for tuition expenses, and the 1098-C for charitable donations of vehicles. Each form is designed to capture specific financial activities that have tax implications.

Understanding the function and requirements of the 1098 tax form is crucial for taxpayers who wish to take advantage of deductions and credits. Not only does it help in reducing taxable income, but it also ensures compliance with federal tax regulations. Therefore, knowing which type of 1098 form you need and how to utilize it properly is a fundamental aspect of tax preparation.

Types of 1098 Tax Forms

1098

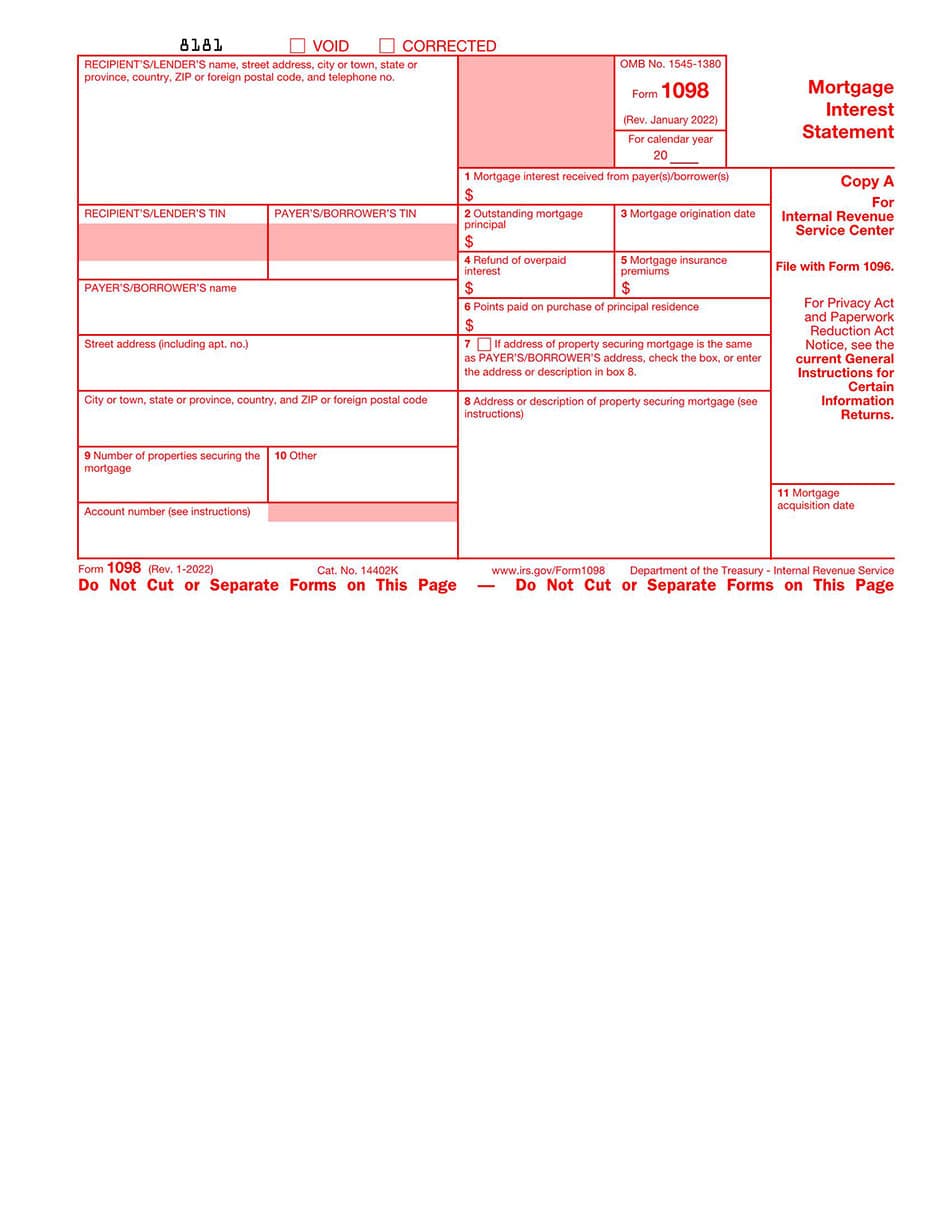

The 1098 form, also known as the Mortgage Interest Statement, is issued by lenders to report mortgage interest of $600 or more received during the year. This form is crucial for homeowners who want to deduct mortgage interest from their taxable income. The 1098 form includes details such as the amount of interest paid, points paid on the mortgage, and any mortgage insurance premiums.

Homeowners can use the information provided on the 1098 form to claim the mortgage interest deduction on Schedule A of their tax returns. This deduction can significantly reduce taxable income, especially for those with substantial mortgage payments. It's important to note that to claim this deduction, taxpayers must itemize their deductions rather than taking the standard deduction.

1098-E

The 1098-E form, or the Student Loan Interest Statement, is used to report interest paid on qualified student loans. Lenders who receive $600 or more in interest payments during the year must provide a 1098-E to the borrower. This form allows taxpayers to claim a deduction for student loan interest, which can reduce their taxable income by up to $2,500.

To qualify for the student loan interest deduction, the taxpayer must have taken out the loan solely to pay qualified education expenses. Furthermore, the taxpayer must be legally obligated to pay the interest on the loan. The deduction is subject to income limits, which means that taxpayers with higher incomes may not qualify for the full deduction.

1098-T

The 1098-T form, also known as the Tuition Statement, is issued by eligible educational institutions to report tuition and related expenses. This form is essential for students or their parents who wish to claim education credits, such as the American Opportunity Credit or the Lifetime Learning Credit. The 1098-T includes information about the amount billed for tuition, scholarships received, and adjustments made for prior years.

Taxpayers can use the 1098-T to determine their eligibility for education credits, which can reduce their tax liability on a dollar-for-dollar basis. It's important to note that the 1098-T does not report payments made, but rather amounts billed. Therefore, taxpayers need to keep accurate records of actual payments made to claim the appropriate credits.

1098-C

The 1098-C form is used to report charitable contributions of motor vehicles, boats, and airplanes. When a taxpayer donates a vehicle to a qualified charity and receives a value of more than $500, the charity must provide a 1098-C. This form includes details about the vehicle, the date of donation, and the fair market value.

Taxpayers can use the information on the 1098-C to claim a deduction for their charitable contribution. However, the deduction is limited to the gross proceeds received by the charity from the sale of the vehicle, unless the charity makes significant use of the vehicle. It's important for taxpayers to obtain the 1098-C within 30 days of the sale or donation to ensure they can claim the deduction.

Who Needs to File a 1098 Tax Form?

The obligation to file a 1098 tax form generally falls on the institution or entity that receives the interest payments, tuition, or charitable contributions. This includes:

- Mortgage lenders who receive $600 or more in mortgage interest payments from a borrower.

- Student loan servicers who receive $600 or more in interest payments from a borrower.

- Educational institutions that receive qualified tuition and related expenses from students.

- Charitable organizations that receive vehicle donations valued over $500.

For taxpayers, the role is to ensure they receive the 1098 tax forms from these entities and accurately report the information on their tax returns. Failure to file these forms can result in penalties for the institutions, while taxpayers might miss out on valuable deductions if they do not receive or properly use the forms.

How to Fill Out a 1098 Tax Form?

While the responsibility of filling out a 1098 tax form lies with the lender or institution, understanding the components can help taxpayers verify the information. Here's a breakdown of the key fields:

- Payer's Information: Includes the name, address, and Taxpayer Identification Number (TIN) of the entity issuing the form.

- Recipient's Information: The taxpayer's name, address, and Social Security Number (SSN) or Taxpayer Identification Number (TIN).

- Interest Paid: The total interest amount received by the payer, which is reported in Box 1 for mortgage interest and Box 1 for student loan interest.

- Mortgage Insurance Premiums: Reported in Box 5 for mortgage interest, if applicable.

- Points Paid: Any points paid on the mortgage, reported in Box 2 for mortgage interest.

- Tuition and Related Expenses: For the 1098-T, the amount billed for qualified tuition and related expenses is reported in Box 1.

- Scholarships or Grants: Also on the 1098-T, reported in Box 5.

Taxpayers should carefully review the information on the 1098 form for accuracy and report it correctly on their tax returns. Any discrepancies should be addressed with the issuing entity to avoid potential issues with the IRS.

When Do You Receive a 1098 Tax Form?

Typically, taxpayers receive their 1098 tax forms by January 31st of each year. This deadline ensures that taxpayers have sufficient time to incorporate the information into their tax returns, which are due by April 15th. Lenders and institutions are required by the IRS to send these forms by the January deadline to facilitate timely tax filing.

If you have not received a 1098 form by the end of January, it's advisable to contact the issuing entity. Delays can happen, but it's important to ensure you have all necessary documentation before filing your taxes. Keep in mind that even if you do not receive a form, you are still responsible for reporting the relevant interest or expenses on your tax return.

How Does the 1098 Tax Form Affect Your Taxes?

The 1098 tax form can have a significant impact on your taxes by enabling you to claim deductions that reduce your taxable income. Here's how each type of 1098 form affects your tax situation:

- 1098 (Mortgage Interest): Allows you to deduct mortgage interest and mortgage insurance premiums if you itemize deductions, which can lower your taxable income.

- 1098-E (Student Loan Interest): Provides a deduction for student loan interest, reducing your taxable income by up to $2,500.

- 1098-T (Tuition Statement): Helps determine eligibility for education credits, such as the American Opportunity Credit or the Lifetime Learning Credit, which directly reduce your tax liability.

- 1098-C (Charitable Contributions): Allows you to deduct the fair market value of donated vehicles, subject to certain conditions, reducing your taxable income.

Each of these deductions and credits has specific rules and limitations, so it's important to understand how they apply to your situation. Properly utilizing the information on the 1098 forms can lead to substantial tax savings.

Common Mistakes to Avoid with 1098 Tax Forms

When dealing with 1098 tax forms, taxpayers often make mistakes that can result in inaccurate tax filings or missed deductions. Here are some common pitfalls to watch out for:

- Not Itemizing Deductions: To benefit from the mortgage interest deduction, you must itemize deductions. Many taxpayers miss out on this benefit by opting for the standard deduction without calculating which option provides the larger tax benefit.

- Ignoring Income Limits: The student loan interest deduction and education credits have income limits. Ensure you meet the eligibility criteria before claiming these deductions.

- Overlooking Adjustments: For the 1098-T, ensure you account for adjustments to prior year tuition that may affect your eligibility for education credits.

- Failing to Verify Information: Always double-check the information on your 1098 forms for accuracy. Incorrect details can lead to issues with the IRS.

- Not Keeping Records: Retain copies of all 1098 forms and relevant documentation. This is crucial in case of IRS inquiries or audits.

Avoiding these mistakes requires careful attention to detail and a thorough understanding of how 1098 forms interact with the tax code. When in doubt, consulting a tax professional can provide valuable guidance.

What Happens If You Don't Receive a 1098 Tax Form?

If you do not receive a 1098 tax form, it does not absolve you of the responsibility to report the relevant interest or expenses on your tax return. Here's what you should do:

- Contact the Issuer: Reach out to the lender, educational institution, or charity to request a copy of the form.

- Use Alternative Documentation: If you cannot obtain the form, use alternative records such as loan statements or receipts to calculate the amounts for your tax return.

- Report the Information: Accurately report the interest or expenses on your tax return even if you do not have the official 1098 form.

Failing to report these amounts can result in penalties or missed deductions, so it's essential to take proactive steps to obtain the necessary documentation.

How to Correct a Mistake on a 1098 Tax Form?

If you discover an error on your 1098 tax form, it's important to address it promptly to prevent issues with your tax filing. Here's how to handle mistakes:

- Contact the Issuer: Notify the entity that issued the form about the mistake. They can issue a corrected form with the accurate information.

- Amend Your Tax Return: If you've already filed your tax return with the incorrect information, you may need to file an amended return using Form 1040-X to correct the error.

- Keep Documentation: Retain copies of the corrected form and any correspondence with the issuer for your records.

Timely correction of errors helps avoid complications with the IRS and ensures you receive the correct tax benefits.

Impact of 1098 Tax Forms on Mortgage Deductions

The 1098 tax form plays a crucial role in determining mortgage deductions, which can significantly reduce taxable income for homeowners. Here's how it impacts your mortgage deductions:

- Interest Deduction: The mortgage interest reported on the 1098 form is deductible if you itemize deductions. This can lead to substantial tax savings, especially for those with large mortgage balances.

- Mortgage Insurance Premiums: Mortgage insurance premiums reported on the 1098 form may also be deductible, providing further tax relief.

- Points Deduction: Points paid on the mortgage may be deductible in the year paid, or over the life of the mortgage, depending on the circumstances.

To maximize the benefits of these deductions, it's crucial to understand the requirements and limitations, such as the need to itemize and the cap on mortgage interest for loans over certain amounts.

Student Loan Interest Deductions and 1098-E

The 1098-E form is essential for claiming the student loan interest deduction, which can reduce your taxable income by up to $2,500. Here's what you need to know:

- Eligibility: You must be legally obligated to pay interest on a qualified student loan, and the loan must be for qualified education expenses.

- Income Limits: The deduction is phased out for taxpayers with modified adjusted gross incomes above certain thresholds.

- Maximum Deduction: The maximum deduction is $2,500, which can lead to significant tax savings.

By carefully reviewing the information on your 1098-E form and understanding the eligibility requirements, you can take full advantage of this valuable deduction.

Education Expenses and 1098-T

The 1098-T form is pivotal in claiming education credits, which can reduce your tax liability on a dollar-for-dollar basis. Here's how to navigate the 1098-T:

- Qualified Expenses: The form reports tuition and related expenses, which are used to determine eligibility for the American Opportunity Credit or the Lifetime Learning Credit.

- Credits: The American Opportunity Credit can provide up to $2,500 per student, while the Lifetime Learning Credit offers up to $2,000 per tax return.

- Record Keeping: Since the 1098-T reports amounts billed, keep records of actual payments to accurately claim the credits.

Understanding the intricacies of the 1098-T form and education credits can lead to significant tax savings for students and their families.

Vehicle Donations and 1098-C

The 1098-C form is used to report charitable donations of vehicles, and understanding it is key to claiming deductions for these contributions:

- Valuation: The deduction is typically limited to the gross proceeds received by the charity from the sale of the vehicle.

- Significant Use: If the charity makes significant use of the vehicle, the deduction may be based on the fair market value.

- Timeliness: Obtain the 1098-C within 30 days of the sale or donation to ensure you can claim the deduction.

By following the guidelines for vehicle donations and ensuring accurate reporting on the 1098-C, taxpayers can maximize their charitable contribution deductions.

FAQs About the 1098 Tax Form

Here are some frequently asked questions about the 1098 tax form:

- Can I claim a deduction without a 1098 form? Yes, you can use other documentation to substantiate your deduction, but having the 1098 form simplifies the process.

- What if my lender doesn't send a 1098 form? Contact them to request the form and use your loan statements to report the interest if necessary.

- How do I know if I'm eligible for education credits? Review the 1098-T form and ensure you meet the criteria for the American Opportunity Credit or Lifetime Learning Credit.

- Can I deduct mortgage interest if I take the standard deduction? No, mortgage interest deductions require itemizing deductions on your tax return.

- What should I do if I find an error on my 1098 form? Contact the issuer to correct the mistake and consider filing an amended tax return if necessary.

- Do I need to keep my 1098 forms? Yes, retain copies of all 1098 forms and related documentation for your records and potential audits.

Conclusion

The 1098 tax form is an essential tool for taxpayers seeking to maximize their deductions and credits. By understanding the different types of 1098 forms, their requirements, and how they impact your taxes, you can ensure accurate tax filings and potentially substantial savings. Whether it's mortgage interest, student loan interest, education expenses, or vehicle donations, the 1098 tax form provides the necessary documentation to claim valuable tax benefits. By avoiding common mistakes, addressing any errors promptly, and consulting a tax professional when needed, you can navigate the complexities of the 1098 tax form with confidence.

For further reading and official guidelines, visit the IRS website to access detailed information and resources on the 1098 tax form.

You Might Also Like

JCPenney Wiki: A Comprehensive Guide To The Retail Giant's LegacyFahad Siddiqui Business: A Transformative Visionary In The Corporate World

Mastering The VW Squeeze Chart: A Complete Guide To Optimize Your Trading Strategy

Bo Burnham Country Music: A Surprising Twist On The Genre

Prospects Of A $120,000 Salary: Is It A Good Income?

Article Recommendations

- Is Kadeem Hardison Married Everything You Need To Know

- Delving Into The Charm Of Ham The Sandlot A Nostalgic Dive Into A Classic

- Kenya A Land Of Rich Heritage And Vibrant Culture