"NerdWallet: How Much House Can I Afford?" is a keyword phrase used to refer to an online calculator provided by NerdWallet, a personal finance website. The calculator is designed to help individuals determine how much they can afford to spend on a home based on their income, expenses, and other financial factors. It takes into account various metrics such as debt-to-income ratio, down payment amount, and interest rates to provide an estimate of the maximum affordable mortgage amount.

Using this calculator can be beneficial for individuals who are considering buying a home, as it provides them with a starting point for budgeting and planning their finances. It can help them avoid overextending themselves financially and ensure that they are able to comfortably afford their mortgage payments and other housing expenses.

To use the calculator, individuals simply need to input their income, expenses, and other relevant financial information. The calculator will then generate an estimate of the maximum affordable mortgage amount, along with a breakdown of the monthly mortgage payments and other costs associated with homeownership.

It's important to note that the calculator's estimate is just thatan estimate. The actual amount that an individual can afford to spend on a home may vary depending on their specific circumstances and financial goals. It is always advisable to consult with a financial advisor or mortgage lender to get personalized advice and guidance on home affordability.

NerdWallet

When it comes to determining how much house you can afford, there are several key aspects to consider. These factors play a crucial role in assessing your financial readiness for homeownership and ensuring that you make an informed decision.

- Income: Your income is a primary determinant of your borrowing capacity. Lenders will evaluate your income to assess your ability to repay the mortgage.

- Debt: Your existing debt obligations, such as credit card balances and car loans, can impact your affordability. Lenders consider your debt-to-income ratio to determine how much additional debt you can handle.

- Down Payment: The amount you can put down on a home will affect your monthly mortgage payments and the total cost of the loan. A larger down payment reduces your loan amount and lowers your interest charges.

- Interest Rates: Interest rates on mortgages fluctuate over time and can significantly impact your monthly payments. Consider current interest rates and how they might affect your affordability.

- Property Taxes: Property taxes vary by location and can be a substantial expense. Factor in property taxes when calculating your monthly housing costs.

- Homeowners Insurance: Homeowners insurance protects your home and belongings in case of damage or loss. The cost of insurance will vary depending on the value of your home and its location.

- HOA Fees: If you're buying a home in a homeowners association (HOA), you may have to pay monthly or annual HOA fees. These fees cover common area maintenance and amenities.

Understanding these key aspects is essential for making informed decisions about homeownership. By carefully considering your financial situation and these factors, you can determine how much house you can comfortably afford and avoid overextending yourself financially.

1. Income

When it comes to determining how much house you can afford, your income plays a pivotal role. Lenders will thoroughly evaluate your income to assess your ability to make timely mortgage payments and manage your overall debt obligations.

- Stable Income: Lenders prefer borrowers with a stable income history, as it indicates your ability to consistently meet your financial commitments. This could include income from employment, self-employment, or investments.

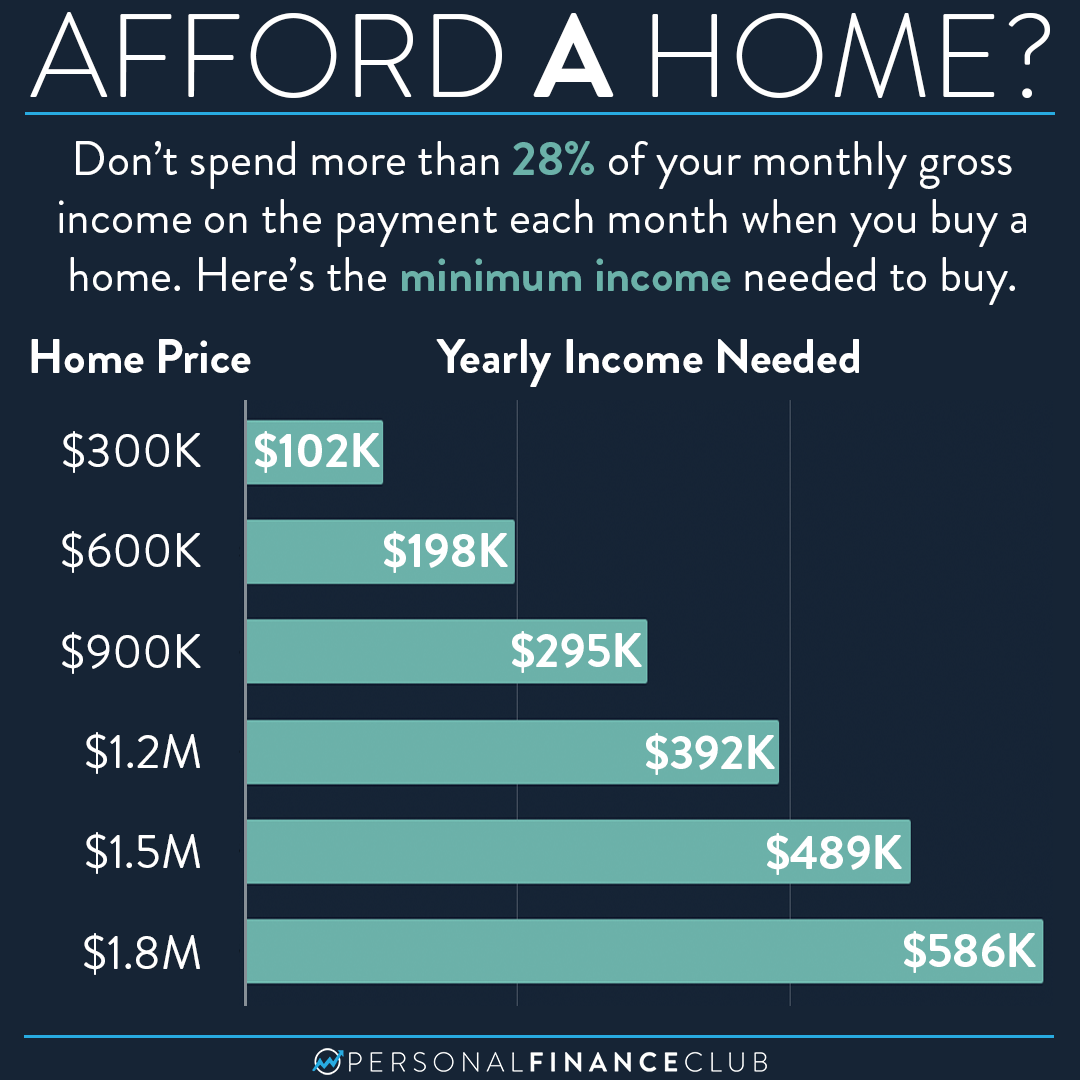

- Debt-to-Income Ratio: Your debt-to-income ratio (DTI) measures how much of your monthly income is allocated towards debt payments. Lenders typically look for a DTI below 36%, indicating that you have sufficient income to cover your housing expenses and other financial obligations.

- Income Verification: To verify your income, lenders will typically request documentation such as pay stubs, tax returns, or bank statements. This helps them assess the accuracy and stability of your income.

- Income Growth Potential: Lenders may also consider your potential for income growth in the future. If you have a history of steady income growth or are in a high-growth industry, this could increase your borrowing capacity.

In summary, your income is a crucial factor in determining how much house you can afford. A stable income, low DTI, and strong income growth potential can all contribute to a higher borrowing capacity and allow you to qualify for a larger mortgage.

2. Debt

Your existing debt obligations play a critical role in determining how much house you can afford through "NerdWallet: How Much House Can I Afford?". Lenders use your debt-to-income ratio (DTI) to assess your ability to manage additional debt, including a mortgage.

DTI is calculated by dividing your monthly debt payments by your monthly gross income. Lenders typically prefer a DTI below 36%, indicating that you have sufficient income to cover your housing expenses and other financial obligations. If your DTI is too high, you may not qualify for a mortgage or may only qualify for a smaller loan amount.

For example, if your monthly gross income is $5,000 and your monthly debt payments total $1,000, your DTI would be 20%. This DTI is considered favorable by lenders and would likely allow you to qualify for a larger mortgage amount.

However, if your monthly debt payments were $1,800, your DTI would be 36%. This higher DTI could make it more difficult to qualify for a mortgage or may result in a lower loan amount.

Therefore, it is important to manage your existing debt obligations wisely to improve your DTI and increase your borrowing capacity when it comes to purchasing a home.

3. Down Payment

When it comes to "NerdWallet: How Much House Can I Afford?", the down payment plays a crucial role in determining your monthly mortgage payments and the overall cost of your loan. A larger down payment can significantly reduce your financial burden in several ways:

- Reduced Loan Amount: A larger down payment means you'll need to borrow less money from the lender. This results in a smaller loan amount, which translates into lower monthly mortgage payments.

- Lower Interest Charges: A larger down payment also reduces the amount of interest you'll pay over the life of the loan. This is because the interest rate is calculated as a percentage of the loan amount. A smaller loan amount means less interest to pay.

- Improved Loan Terms: A larger down payment can improve your loan terms, such as securing a lower interest rate or obtaining a shorter loan term. This can further reduce your monthly payments and save you money in the long run.

- Increased Equity: A larger down payment gives you a higher equity stake in your home from the start. This can provide a financial cushion in case of unexpected events or if you decide to sell your home in the future.

In summary, a larger down payment can significantly reduce your monthly mortgage payments, lower your overall loan costs, and improve your financial position as a homeowner. Therefore, it's important to consider saving for a substantial down payment when planning to purchase a home.

4. Interest Rates

Interest rates play a crucial role in determining "NerdWallet: How Much House Can I Afford?". Mortgage interest rates fluctuate over time, and even small changes can have a significant impact on your monthly mortgage payments and overall housing costs.

For example, let's say you're considering a $200,000 mortgage with a 30-year term. If the interest rate is 3%, your monthly payment would be approximately $843. However, if the interest rate increases to 4%, your monthly payment would jump to $934a difference of $91 per month.

Over the life of the loan, the higher interest rate would result in you paying $32,760 more in interest charges. This highlights the importance of considering current interest rates and how they might affect your affordability when using "NerdWallet: How Much House Can I Afford?".

When interest rates are low, it can be a good time to consider buying a home, as you may be able to secure a lower monthly payment and save money on interest charges over time. However, it's important to remember that interest rates can change, so it's essential to factor in potential increases when determining how much house you can afford.

5. Property Taxes

Property taxes are an important consideration when determining how much house you can afford through "NerdWallet: How Much House Can I Afford?". Property taxes vary significantly by location and can add a substantial amount to your monthly housing expenses.

When using "NerdWallet: How Much House Can I Afford?", it's crucial to factor in property taxes to get an accurate estimate of your monthly housing costs. These taxes are typically paid annually or semi-annually, and the amount is determined by the assessed value of your property and the local tax rate.

For example, if you're considering buying a home in an area with high property taxes, your monthly housing costs could be significantly higher than in an area with lower taxes. This difference could impact your affordability and may require you to adjust your budget accordingly.

To avoid unexpected expenses, it's essential to research property taxes in the areas you're considering and factor them into your calculations when using "NerdWallet: How Much House Can I Afford?". This will help you make an informed decision and ensure that you can comfortably afford the ongoing costs of homeownership.

6. Homeowners Insurance

In the context of "NerdWallet: How Much House Can I Afford?", homeowners insurance plays a crucial role in determining the overall cost of homeownership. It provides financial protection against unexpected events that could damage or destroy your property and belongings.

- Coverage and Protection: Homeowners insurance offers a wide range of coverage options to protect your home, including damage from fire, theft, vandalism, and natural disasters. This coverage ensures that you can repair or replace your property and belongings if they are damaged or lost.

- Financial Security: Homeowners insurance provides financial security by covering the costs of repairs or replacements, preventing you from having to pay out-of-pocket expenses that could be financially devastating.

- Mortgage Requirement: Most mortgage lenders require homeowners to have homeowners insurance as a condition of the loan. This protects the lender's investment in the property and ensures that the home is adequately protected.

- Cost Considerations: The cost of homeowners insurance varies depending on factors such as the value of your home, its location, and the coverage options you choose. It's important to consider these costs when determining how much house you can afford, as they can impact your monthly housing expenses.

Overall, homeowners insurance is an essential component of homeownership and should be factored into your financial planning when using "NerdWallet: How Much House Can I Afford?". It provides peace of mind and financial protection, ensuring that you are prepared for unexpected events that could impact your home and belongings.

7. HOA Fees

When considering "nerdwallet how much house can I afford", HOA fees are an important factor to take into account. HOA fees are charged by homeowners associations to cover the costs of maintaining common areas and amenities within a community. These fees can vary depending on the size and amenities of the community, and can add to your monthly housing expenses.

- Community Maintenance: HOA fees are used to maintain common areas such as landscaping, pools, clubhouses, and other amenities. This ensures that these areas are well-maintained and visually appealing, which can enhance the overall value and desirability of the community.

- Property Value: Homes in communities with active HOAs tend to have higher property values compared to those without HOAs. This is because HOAs enforce certain standards and regulations, such as architectural guidelines and landscaping requirements, which help maintain the overall aesthetic and value of the neighborhood.

- Shared Amenities: HOA fees provide access to shared amenities that individual homeowners may not be able to afford or maintain on their own. These amenities can include swimming pools, fitness centers, clubhouses, and walking trails, which can enhance the quality of life for residents.

- Community Involvement: HOAs often organize community events and activities, which can foster a sense of belonging and camaraderie among residents. This can be especially beneficial for families with children or individuals who value social interaction.

While HOA fees can provide certain benefits and enhance the overall livability of a community, it's important to factor these costs into your budget when using "nerdwallet how much house can I afford". HOA fees can vary significantly, so it's essential to research the specific HOA fees associated with the community you're considering before making a purchase decision.

Frequently Asked Questions about "NerdWallet

This section addresses common questions and concerns individuals may have when using "NerdWallet: How Much House Can I Afford?" to determine their home affordability.

Question 1: What factors are considered when determining how much house I can afford?

Answer: "NerdWallet: How Much House Can I Afford?" considers various factors, including your income, debt obligations, down payment amount, interest rates, property taxes, homeowners insurance costs, and HOA fees (if applicable).

Question 2: How does my income impact my affordability?

Answer: Your income is a primary determinant of your borrowing capacity. Lenders evaluate your income to assess your ability to make timely mortgage payments and manage your overall debt.

Question 3: What is a debt-to-income ratio, and how does it affect my affordability?

Answer: Your debt-to-income ratio (DTI) measures how much of your monthly income is allocated towards debt payments. Lenders typically prefer a DTI below 36%, indicating that you have sufficient income to cover your housing expenses and other financial obligations.

Question 4: How much should I save for a down payment?

Answer: A larger down payment can significantly reduce your monthly mortgage payments and the overall cost of your loan. Aim to save at least 20% of the home's purchase price for a down payment to avoid private mortgage insurance (PMI).

Question 5: How do interest rates affect my affordability?

Answer: Interest rates on mortgages fluctuate over time and can significantly impact your monthly payments. Consider current interest rates and how they might affect your affordability, as even small changes can have a substantial impact on your budget.

Question 6: Are there any additional costs to consider besides the mortgage payment?

Answer: Yes, in addition to your mortgage payment, you will also need to factor in property taxes, homeowners insurance, and possibly HOA fees (if applicable). These additional costs can vary depending on your location and the property itself, so it's important to include them in your affordability calculations.

By understanding these key factors and addressing common questions, individuals can use "NerdWallet: How Much House Can I Afford?" with confidence to make informed decisions about their homeownership journey.

Transition to the next article section: Understanding these factors and addressing common questions can help you make informed decisions when determining how much house you can afford. The next section will provide additional insights into the home affordability process.

Tips for Using "NerdWallet

Determining how much house you can afford is a crucial step in the homebuying process. "NerdWallet: How Much House Can I Afford?" provides a valuable tool to help you assess your financial readiness and make informed decisions. Here are some tips to help you get the most out of this tool:

Tip 1: Gather your financial information. Before you start using the calculator, gather all necessary financial information, including your income, debt obligations, and savings. This will ensure that you have a clear picture of your financial situation.

Tip 2: Be honest about your expenses. When entering your expenses into the calculator, be honest about your spending habits. Underestimating your expenses can lead to an inaccurate estimate of your affordability.

Tip 3: Consider your future financial goals. Homeownership is a long-term commitment. When determining how much house you can afford, consider your future financial goals, such as saving for retirement or funding your children's education.

Tip 4: Get pre-approved for a mortgage. Getting pre-approved for a mortgage can give you a better understanding of your borrowing capacity and strengthen your position when making an offer on a home.

Tip 5: Use the calculator as a starting point. The estimate provided by "NerdWallet: How Much House Can I Afford?" is just a starting point. It's important to consult with a financial advisor or mortgage lender to get personalized advice and guidance.

By following these tips, you can use "NerdWallet: How Much House Can I Afford?" effectively to determine your affordability and make informed decisions about your homeownership journey.

Conclusion

Determining "How Much House Can I Afford?" is critical for responsible homeownership. "NerdWallet: How Much House Can I Afford?" provides a comprehensive tool to assess affordability, considering income, expenses, and other financial factors. By understanding the key aspects of affordability, individuals can make informed decisions about their homebuying journey.

Remember, affordability is not just about the monthly mortgage payment. It's about ensuring that housing costs align with your overall financial goals and long-term well-being. By carefully evaluating your financial situation and using tools like "NerdWallet: How Much House Can I Afford?", you can make a confident decision about homeownership that sets you up for financial success.

You Might Also Like

Unleash The Magic With JoJo Siwa Flash: A Dazzling Dance AdventureDiscover The Dynamic Duos: 2 Chainz's Unforgettable Music Collaborations

Unleash Extreme Volume With Our Revolutionary Shocking Volume Hair Spray

Explore The World Of Jack De Sena: Discover His Age And More

The Ultimate Mash Rules Guide For Homebrewers

Article Recommendations

- All You Need To Know About Naval Air Station Lemoore

- Height Of Amanda Seyfried A Detailed Look At Her Stature And More

- Michael Parker A Closer Look At His Life Achievements And Legacy